The taxation of capital gains on financial assets

When and how should you value

your unlisted shares?

Capital gains on financial assets realised as from 1 January 2026 will be subject to a 10% tax, with some exceptions.

Here is everything you need to know to anticipate and optimise your situation.

What does la loi du 6 avril 2026 ?

Here are the main provisions

Entrée en vigueur le 1ᵉʳ janvier 2026, la loi du 6 avril 2026 introduit la taxation des plus-values sur actifs financiers. Dans certains cas, comme les actions de sociétés cotées, les institutions financières feront les calculs. Par contre, pour les sociétés non cotées en bourse, il est important d’en avoir une évaluation au 31 décembre 2025, pour figer et certifier la valeur de départ.

For listed shares or assets managed by banks (for example private equity funds), it is the institutions that must calculate and withhold the tax. However, by exception, the taxpayer may choose to do it themselves and declare the capital gain in their tax return. This is what is known as the “opt-out”.

The persons concerned are individuals, non-profit organisations and foundations. Companies, whose capital gains are taxable (with some exceptions), are not subject to this tax.

Assets concerned: shareholdings (listed or unlisted), bonds, ETFs, derivatives, cryptocurrencies, currencies, capitalisation or life insurance contracts, etc., except savings products.

Only realised capital gains are taxed.Example: an inheritance without a sale of assets does not trigger the tax.

Les 3 régimes de taxation

La réforme fiscale sur les plus-values financières distingue trois situations d’imposition.

The specific regime for internal capital gains applies to taxpayers who sell shares in a company to another company they control. In this case, capital gains are taxed at 33%.

The general regime mainly concerns stock market investors whose capital gains are taxed at 10%. However, they benefit from an exemption of €10,000 per year, which can be increased by €1,000 each year, with a maximum carry-forward period of 5 years.

The regime for “substantial” shareholdings of at least 20% of a company’s share capital. These benefit from an exemption of €1,000,000 per five-year period, as explained in more detail on this page.

It is in this situation that investors, including entrepreneurs, have an interest in having a reasoned valuation report of the value of each shareholding as at 31 December 2025, prepared by a certified accountant or statutory auditor.

What are the exemptions?

Each taxpayer benefits from an annual allowance of €10,000.

Capital gains realised on significant shareholdings at least 20% of a company’s share capital) are exempt up to €1,000,000 per five-year period, provided that this shareholding was held at some point during the 10 years preceding the sale.

This allowance can be increased by €1,000 per year, with a ceiling of €5,000 every five years.

In the event of a merger or demerger,the unrealised capital gain is also exempt.

Tip: The annual exemption of €10,000 is not automatic.

It must be explicitly claimed in the tax return. The unused portion can be carried forward for one year only.

How is the tax base calculated?

The taxable base is calculated as the difference between the sale value of the asset and

its reference acquisition value, excluding transaction costs.

Determination of the reference value as at 31/12/2025

The reference value of listed securities is that of 31 December 2025. However, until 31 December 2030, you may prove that you acquired them at a higher price. For your unlisted securities,you may choose the highest amount resulting from one of the following four methods: :

Method 1: a recent transaction

You can prove the price of a purchase, a sale or a capital increase in 2025.

Method 2: a call or put option

You can prove that you signed or exercised a call or put option in 2025. Reference will be made to the law of 26 March 1999.

Method 3: the accounting lump-sum method

You may choose the amount resulting from the following formula: equity as at 31 December 2025 plus four times EBITDA. However, be careful: this may not be the formula that offers you the best protection.

Method 4: a certified accountant’s report

You may also refer to a valuation report specifically prepared by a certified accountant or an independent statutory auditor.

This report will take into account the context of your company and any latent capital gains not reflected in the balance sheet. In most cases, it will be enforceable against the tax authorities.

This is certainly the approach to favour when consulting a specialist in the field.

Valuation example:

Let us take the simplified example of a company owned by six cousins, whose equity as at 31 December 2025 amounts to €1,000,000, including a property recorded in the accounts for €400,000.

The EBITDA is €50,000. According to the lump-sum formula, the company is valued at €1,200,000 at the reference date.

In reality, if a certified accountant demonstrates that the market value of the property is €1,000,000, they may value the company at €1,650,000.

In the event of a sale at a price higher than the lump-sum value, the report would therefore avoid nearly €40,000 in tax for the shareholders. This is not insignificant and provesthat one should not limit oneself to the lump-sum formula.

The 10% capital gains tax will sometimes be significant. That is why, in many situations, obtaining a valuation from an experienced and independent financial professional will contribute to your legal and financial security.

A Tax calculation summary

The taxable base is calculated as the difference between the sale value of the asset and

its reference acquisition value, excluding transaction costs.

Capital losses are deductible within the same asset category and can be carried forward for 1 year.

A general exemption of €10,000 per year,index-linked and increaseable up to €15,000.

Capital Significant shareholdings of at least 20% benefit from a tax exemption of up to €1,000,000 every five years. Beyond that, the applicable tax rates are shown in the table below:

Tip: if you own shares in unlisted companies, consult a certified accountant (or statutory auditor), ideally experienced in valuation. Avoid losing money, and use the right method.

Talk to a specialist today!

Why entrust us with the valuation of your shareholdings?

1. Our certifications

Charles Markowicz is a certified ITAA accountant and a court-appointed expert listed in the federal register.

2. Our experience

Whether for court proceedings in the event of shareholder disputes or for private engagements, we apply a proven methodology and take into account the specific circumstances and context explained by our clients.

3. Your security

A report prepared by an experienced professional reduces the risk of having to pay too much tax.

4. Avoiding mistakes

By not choosing the right valuation method, you may regret it at the time of the sale.

5. A useful and reliable report

The reports we prepare are fully reasoned and can be used as supporting evidence for the values claimed vis-à-vis the tax authorities.

6. Your interests come first

Our aim is to provide you with the best possible benchmark, in the short, medium and long term.

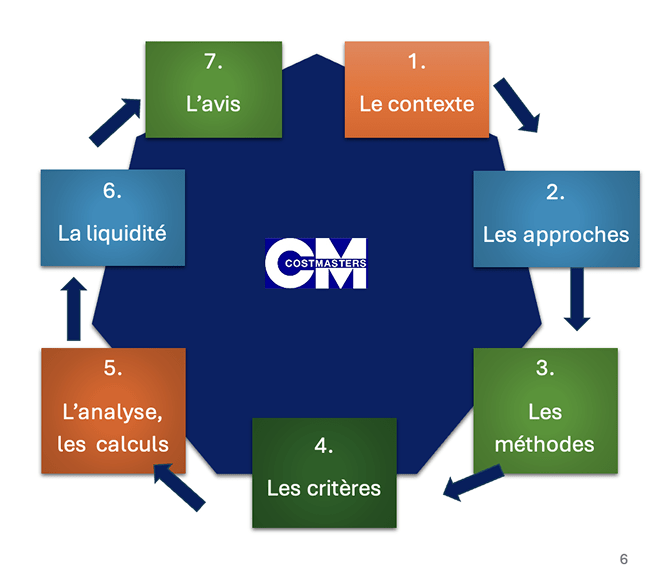

How we value

your company and your shareholdings

It is easy to make mistakes when valuing a company by relying on unrealistic assumptions that can prove costly later on. Since every situation is different, valuing a company requires a specific focus. We do not use off-the-shelf formulas, but apply financial theory to the specific context of the valuation.

We take several valuation approaches into account and analyse them using methods recognised in Belgium, sometimes developed by international experts and professors. Since an SME is not a large corporation, we also take this into account in our work. This results in a technical expert opinion that you can use in various situations depending on its purpose.

This is what ensures reasonable and contextualised valuations.

Your frequent asked questions

By transferring your financial assets during your lifetime, you may risk bringing your shareholdings below the 20% threshold required to benefit from the exemption of up to €1,000,000. This should therefore be included in your estate and tax planning strategy. It is also possible to reorganise the shareholding structure of one or more companies so that there are no longer any shareholders holding less than 20%. In some cases, transfers between shareholders may be of interest to them, beyond the capital gains tax issue.

Let us first recall that a holding company is a company that owns shareholdings in other companies. If you transfer your shares to a holding company that you own or to a new one to be created, you may risk having your capital gain taxed at 30%, which is not attractive. Another disadvantage is that dividends and capital gains will be received by the holding company and not by you personally, which may result in additional costs and taxation. To extract the money from the holding company, you will have to wait and pay at least 15% withholding tax. A company (holding) may benefit from the RDT regime (definitively taxed income), which avoids double taxation of received dividends. However, it must meet certain holding period and amount (or percentage) conditions. The overall cost and profitability must therefore be assessed globally.

It is commonly believed that the usufructuary collects the income and bears the costs of a property or financial assets, and this is true.

However, in the case we are dealing with here, it is the bare owner who must pay the tax of up to 10%. This is quite logical, because when shares are sold, it is not income that is being received, but rather part of the capital that is being disposed of.

In this case, the legislator considers that it is the owner of the capital who must pay the tax.

That being said, both this and the obligation to provide income to the bare owner can be customised in the splitting agreement. In this respect, you should consult a notary, bank adviser or lawyer.

nous préoccupe ici, c’est le nu-propriétaire qui doit payer la taxe de 10% maximum. C’est assez logique car lorsque l’on vend des actions, ce n’est pas le fruit ou la charge d’entretien que l’on touche mais une partie du capital que l’on entame (un peu comme si on enlève une grosse branche du tronc, on

touche alors à sa productivité). Et dans ce cas, le législateur estime que c’est le propriétaire du capital qui doit payer la taxe. Cependant, tant cela que l’obligation d’assurer un revenu au nu-propriétaire peut être personnalisé lors du démembrement. A ce sujet, consultez un notaire, conseiller bancaire ou avocat.

You will have the following options:

Prove the value of the shares by means of a document evidencing a transaction carried out in 2025 or a sale promise (option) at a determined price. You must pay attention to the details of the offer and prove its authenticity.

Another possibility is to apply the statutory lump-sum formula: the company’s equity plus four times EBITDA. However, this formula may be to your disadvantage if, for any reason, its result is lower than what a certified accountant or statutory auditor would consider to be the company’s value.

You may also rely on a valuation report from an independent financial professional. As there are several approaches and methods to value a company, it is advisable to use the services of a specialist who understands the company and can provide an appropriate valuation.

During the five years following the entry into force of the law, you may also claim a higher reference value than that of 31/12/2025 if you can prove it. This is notably the case if your shares have lost value since their acquisition.

There are several exceptions or exemptions, the main ones being: Each taxpayer (pay attention to your marriage contract, if applicable) benefits from an exemption of €10,000 per year, which can be increased by €1,000 per year, up to five times. Under community of property: €20,000 per year. Under separation of property: €10,000 per year per person. You may offset capital losses against capital gains, but with two limitations: the offset only applies within the same year and within the same category of financial assets. Significant shareholdings in a company, i.e. at least 20% per individual at the time the capital gain is realised, benefit from an exemption of up to €1,000,000 every five years.

Transfers of ownership without consideration, such as a donation or inheritance, are not subject to the 10% tax. However, when the capital gain is eventually realised, it will be calculated based on the original acquisition value, not the value agreed upon at the time of the transfer or inheritance.

Once the exemptions described above have been deducted, the following rates apply:

1.25% from €1,000,001 to €2,500,000

2.25% from €2,500,001 to €5,000,000

5% from €5,000,001 to €10,000,000

10% as from €10,000,001

As a general rule, for assets managed by your bank or insurance company, they calculate and withhold the tax at source.

However, you may also choose the “opt-out”, meaning that you calculate it yourself. The advantage is that you do not have to wait one or two years to deduct capital losses actually incurred.

Financial institutions must send an informative form to the tax authorities, and based on this and what you declare, the amount due will be calculated in your tax assessment notice.

There is no territorial exception. If you are subject to Belgian tax as a resident, your capital gains generated abroad are also taxable.

The FIFO principle applies (First In, First Out). This means that you are deemed to have sold the first shares you acquired, then the next ones, and so on.

Costmasters story has been valuing unlisted shares (especially SMEs) for many years. Our approach is adapted to each situation, as objectives are identified case by case.

We analyse the company from several angles and calculate several values using recognised approaches and methods.

First, we calculate the adjusted net asset value, i.e. the real resources, including off-balance-sheet items, generated or consumed by the company since its creation.

Then, we compare it to other companies using several methods. Finally, we calculate its intrinsic value, which discounts the expected future income.

For each calculation, where relevant, we distinguish between the enterprise value and the equity value, in accordance with applied and explained financial theory.

We then compare the results obtained in order to form an opinion on the company’s value.

Who is Charles Markowicz?

Dirigeant le cabinet d’expertise comptable Costmasters, Charles Markowicz est expert-comptable certifié ITAA, Expert judiciaire et médiateur agréé. Il a une longue expérience de l’évaluation de sociétés, notamment avant ou lors de conflits d’actionnaires, parfois soumis aux Tribunaux.

Drawing on this experience, he is also the co-author of a book on the subject, more specifically the part presenting modern valuation methods for SMEs.

Testimonials

“I highly recommend Costmasters’ services. Their expertise in navigating the complex Belgian tax system and their professionalism in handling my files have been invaluable. They are responsive, rigorous and efficient.”

Marta M.

Self-employed

“I am extremely satisfied with Costmasters’ work. Their accounting expertise is remarkable and helps me understand the complex aspects of my situation. Their responsiveness and availability are greatly appreciated.”

Muriel

Self-employed

“After many years of experience in business, I have never come across an accounting firm with so much expertise, combined with such a strong sense of human values. I can only highly recommend this firm, which truly brings numbers to life.”

Victor H.

Entepreneur

“I highly recommend Costmasters and its team, who handled my case with rigour and professionalism, and always with great kindness.”

Michel C.

Entrepreneur

Don’t wait any longer to have your company valued, whether in anticipation of the capital gains tax or in another context. Contact us if you would like to find out its value.